India's monthly SIP inflows hit ₹29,845 crore in February 2026 — a 15% year-on-year increase — confirming that systematic investing through mutual funds has become genuinely mainstream. Over 10 crore SIP accounts are now active, and the industry crossed ₹3 trillion in annual SIP inflows for the first time in 2025.

But here is the gap most investors never address: nearly all of them run a flat SIP. The same ₹5,000 or ₹10,000 per month that they set up in 2020 or 2022 — unchanged, while their salary has likely grown 30–50%. That stagnant SIP amount is quietly costing them a crore.

The short answer: A step-up SIP starting at ₹5,000/month with a 10% annual increase builds ₹1.06 crore in 20 years at 12% CAGR. A flat ₹5,000/month SIP at the same return builds ₹49.9 lakh. The difference is ₹56.1 lakh — more than double the corpus.

SIP Momentum: ₹29,845 Crore in February 2026

The AMFI data for February 2026 confirms that India's retail SIP investor base is growing and resilient:

| Month | SIP Inflows | Year-on-Year Change | Note |

|---|---|---|---|

| February 2026 | ₹29,845 crore | +15% YoY | Slight dip from Jan due to shorter month |

| January 2026 | ₹31,000+ crore | +18% YoY | Second consecutive month above ₹31K crore |

| December 2025 | ₹31,000+ crore | +17% YoY | First month to cross ₹31K crore ever |

| Full year 2025 | ₹3+ trillion | First time annual SIP crossed ₹3T | Milestone year for Indian mutual funds |

This sustained SIP growth — even during the Sensex correction from 86,159 (December 2025) to ~73,000 (March 2026) — demonstrates that Indian retail investors are maturing. They are not panic-selling during corrections; they are continuing their mandates. That is exactly the right behaviour. But a flat SIP in a growing-income environment is still leaving significant wealth on the table.

What Is a Step-Up SIP and How Does It Work?

A step-up SIP (or top-up SIP) adds one parameter to a regular SIP: an annual increase percentage. Every year — typically on the anniversary date of your SIP — the monthly contribution automatically increases by that percentage.

| Year | Monthly SIP Amount | Annual Contribution | Cumulative Invested |

|---|---|---|---|

| Year 1 | ₹5,000 | ₹60,000 | ₹60,000 |

| Year 2 | ₹5,500 | ₹66,000 | ₹1,26,000 |

| Year 3 | ₹6,050 | ₹72,600 | ₹1,98,600 |

| Year 5 | ₹7,326 | ₹87,912 | ₹3,66,312 |

| Year 10 | ₹11,789 | ₹1,41,468 | ₹9,56,244 |

| Year 15 | ₹18,973 | ₹2,27,676 | ₹19,26,360 |

| Year 20 | ₹30,617 | ₹3,67,404 | ₹34,37,880 |

Notice that by Year 10, you are investing ₹11,789/month — what started as a modest ₹5,000 SIP is now a substantial contribution. But crucially, each of those earlier years' investments has been compounding for 10–15+ years. That compounding head start is what drives the ₹1.06 crore outcome.

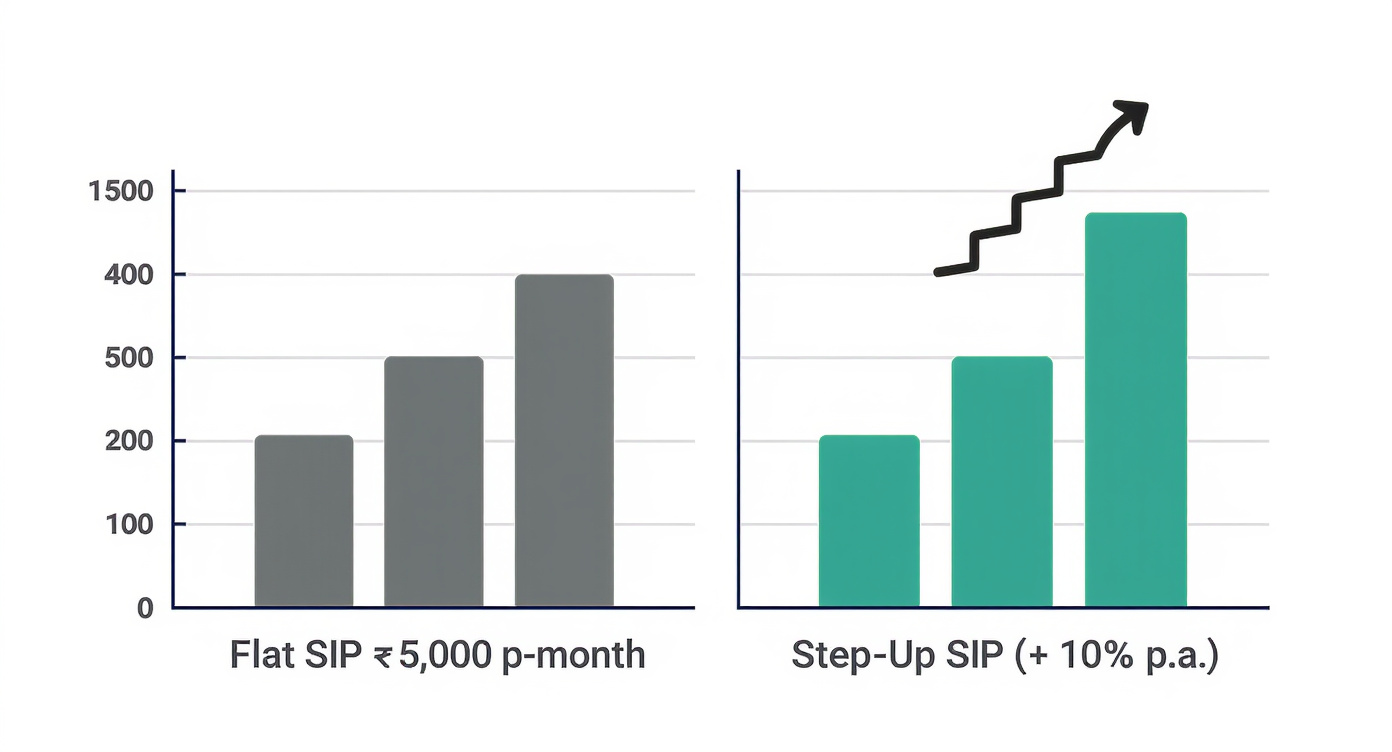

The Maths: ₹1.06 Crore vs ₹49.9 Lakh

The fundamental reason step-up SIPs outperform is simple: more capital deployed earlier, compounding for longer. Here is the full comparison:

Step-Up SIP (₹5,000/month + 10% annual increase) vs Flat SIP (₹5,000/month) — corpus comparison at 10, 15, and 20 years at 12% CAGR. Source: Calculated using UtilsDaily Step-Up SIP Calculator.

| Scenario | 10 Years | 15 Years | 20 Years |

|---|---|---|---|

| Flat SIP ₹5,000/month — Corpus | ₹11.5 lakh | ₹25.0 lakh | ₹49.9 lakh |

| Step-Up SIP (10% p.a.) — Corpus | ₹18.0 lakh | ₹50.1 lakh | ₹1.06 crore |

| Flat SIP — Total Invested | ₹6.0 lakh | ₹9.0 lakh | ₹12.0 lakh |

| Step-Up SIP — Total Invested | ₹9.6 lakh | ₹19.3 lakh | ₹34.4 lakh |

| Extra corpus from step-up | +₹6.5 lakh | +₹25.1 lakh | +₹56.1 lakh |

How ₹5,000/month grows with 10% annual step-up — monthly SIP amount at key milestones. The contribution itself compounds even before market returns are applied.

How Much Should You Step Up — and When?

The practical answer: step up by your salary increment percentage, every April. Here is the framework:

| Your Situation | Recommended Step-Up | 20-Year Corpus (₹5,000 start, 12% CAGR) |

|---|---|---|

| Conservative / modest hike years | 5%–7% p.a. | ₹66–₹78 lakh |

| Standard salary growth | 10% p.a. | ₹1.06 crore |

| High-growth career / above-average hike | 15% p.a. | ₹1.52 crore |

| Variable (step up only in good years) | 5–15% when feasible | Varies, but still significantly beats flat SIP |

April rule: Every year in April, look at your salary increment letter. Take the increment percentage and apply the same increase to your SIP amount. You will not feel the difference in lifestyle — your net take-home also went up — but the compounding impact over 15–20 years is transformative.

How to Use the Step-Up SIP Calculator

The UtilsDaily Step-Up SIP Calculator lets you model any combination of starting SIP amount, annual step-up percentage, expected return, and tenure:

- Starting SIP amount: Enter what you can invest today — even ₹500/month is a valid starting point.

- Annual step-up %: Enter your expected salary growth rate (10% is a reasonable default for India's urban workforce).

- Expected return: 12% is a common long-term assumption for diversified equity funds; use 10% for a conservative estimate.

- Investment tenure: Enter 15–20 years for long-term wealth goals. The step-up effect is most dramatic beyond 12 years.

Use the XIRR Calculator to verify the actual return rate on your existing SIP history — it accounts for the irregular cash flow pattern of a step-up SIP more accurately than simple CAGR. For comparison, model the same total invested amount as a lump sum using the Lumpsum Calculator to see why time-in-market and early deployment beats waiting to accumulate a larger single sum.

The Verdict

- A step-up SIP doubles your 20-year corpus on the same starting investment — ₹1.06 crore vs ₹49.9 lakh at 12% CAGR with a 10% annual step-up.

- April is the ideal month to step up — your salary increment has just been applied, and the new financial year is a natural reset point.

- Any step-up is better than none — even a 5% annual increase adds ₹16 lakh more than a flat SIP at 20 years.

- Start today — the step-up benefit is front-loaded: the earlier you begin the compounding clock, the more each year's additional contribution is worth. Use the Step-Up SIP Calculator to compute your own 20-year number right now.

Sources & Citations

Data sources: AMFI — Monthly SIP Inflow Data (February 2026, March 2026); Free Press Journal — SIP Inflows ₹29,845 Crore (March 2026). All corpus projections calculated using the UtilsDaily Step-Up SIP Calculator and cross-verified against the SIP Calculator.