For everyone born in 1960 or later — which includes all Americans turning 62 today — the Social Security Full Retirement Age is exactly 67. Claiming at 62 does not cut your benefit by "about 30%." It cuts it by exactly 30%, determined by a federal formula that has not changed. And the math behind when to claim is straightforward enough to walk through in this article.

The 2025 Social Security Fairness Act also changed the calculation for roughly 3.1 million public employees, eliminating the WEP and GPO provisions that had reduced benefits for teachers, firefighters, and government workers. If you are in that category, your claiming strategy may have changed meaningfully.

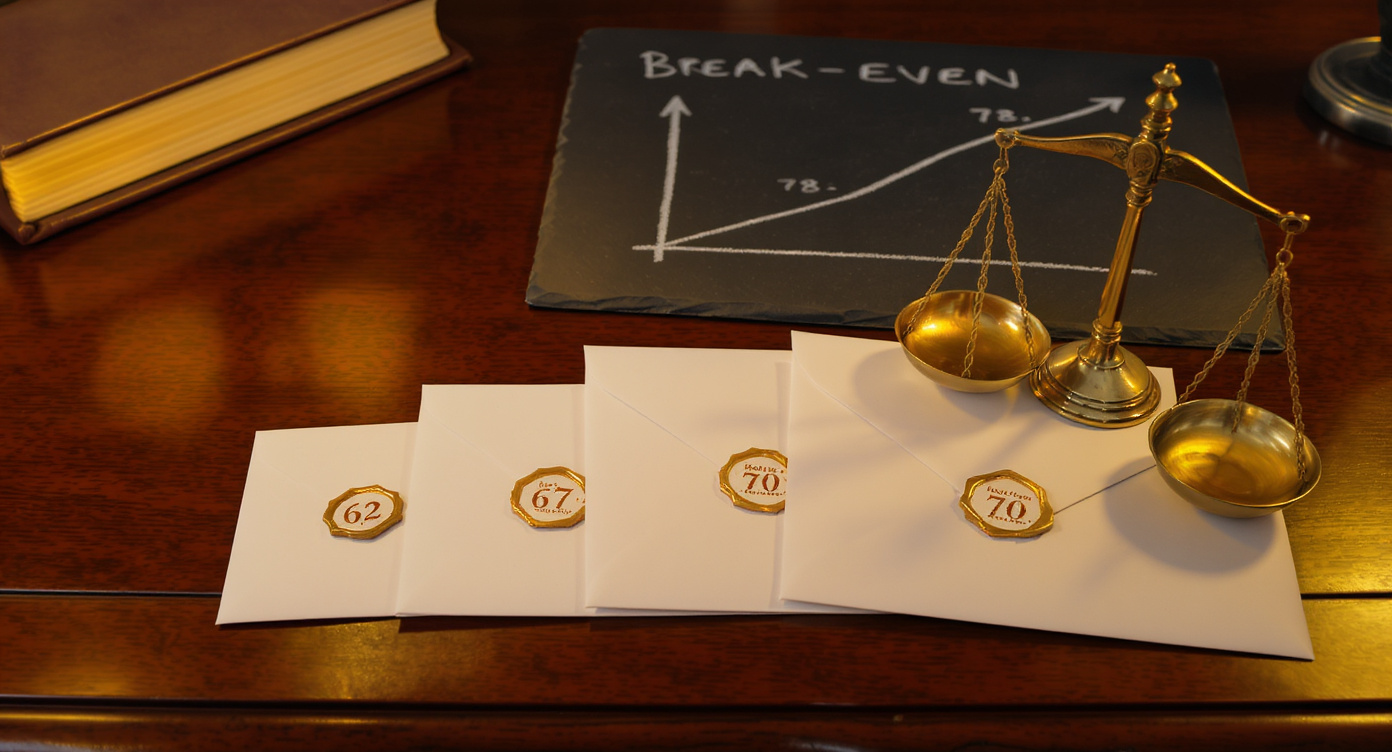

The key numbers: Claiming at 67 (FRA) instead of 62 breaks even at age 78y8m. Claiming at 70 instead of 67 breaks even at age 82y6m. Average American life expectancy at 62 is 81.4 years (male) and 84.3 years (female) — both past the first break-even. The average person comes out ahead by waiting. The exception: if you have reason to expect a significantly shorter lifespan.

How Social Security Benefits Are Calculated

Your Social Security benefit is based on your AIME (Average Indexed Monthly Earnings) — an average of your 35 highest-earning years, adjusted for wage inflation. A formula then converts your AIME into your PIA (Primary Insurance Amount) — the monthly benefit you receive if you claim exactly at your FRA.

For 2026, the maximum PIA figures illustrate the range:

| Claiming Age | Maximum Monthly Benefit (2026) | As % of FRA Benefit |

|---|---|---|

| Age 62 | $2,969/month | 70% of FRA benefit |

| Age 67 (FRA) | $4,207/month | 100% |

| Age 70 | $5,251/month | 124% of FRA benefit |

For all calculations in this article, we use a $1,000 PIA as the baseline — a round number that makes the math transparent and scales to any actual benefit. To find your personalized numbers, log into my Social Security at ssa.gov and view your actual estimated benefit at each claiming age.

Claiming at 62: The Exact 30% Reduction

The SSA reduction formula is not a rounded estimate — it is exact, derived from federal statute. For FRA = 67, claiming at 62 is 60 months early. The formula applies:

- For the first 36 months early (ages 64–67): benefit reduced by 5/9 of 1% per month = 0.5556%/month

- For the next 24 months early (ages 62–64): benefit reduced by 5/12 of 1% per month = 0.4167%/month

36 months × 0.5556% = 20.00%. Plus 24 months × 0.4167% = 10.00%. Total = exactly 30.00%. You receive 70% of your PIA — permanently, for every month you collect. The reduction is not recalculated when you reach 67; it stays at 70% for life.

Monthly Social Security benefit by claiming age at $1,000 PIA (Primary Insurance Amount). FRA = 67 for those born 1960 or later. Reduction formula: 5/9 of 1% per month for first 36 months early + 5/12 of 1% per month for next 24 months. Delayed credits: 2/3 of 1% per month (8%/year) past FRA up to age 70. Source: SSA.gov quickcalc/earlyretire.html; SSA.gov delayret.html — exact formula calculations, not approximations.

| Claiming Age | Months from FRA | Reduction/Credit | % of PIA | Monthly Benefit ($1,000 PIA) |

|---|---|---|---|---|

| 62 | 60 months early | −30.00% | 70.00% | $700 |

| 63 | 48 months early | −25.00% | 75.00% | $750 |

| 64 | 36 months early | −20.00% | 80.00% | $800 |

| 65 | 24 months early | −13.33% | 86.67% | $867 |

| 66 | 12 months early | −6.67% | 93.33% | $933 |

| 67 (FRA) | 0 | None | 100.00% | $1,000 |

| 68 | 12 months late | +8.00% | 108.00% | $1,080 |

| 69 | 24 months late | +16.00% | 116.00% | $1,160 |

| 70 | 36 months late | +24.00% | 124.00% | $1,240 |

The permanence matters: The 30% reduction at 62 is not just for the years before 67. It is a permanent lifetime reduction. If your FRA benefit would have been $1,800/month, claiming at 62 gives you $1,260/month — for every month you live. That $540 monthly gap, at 2.8% COLA, compounds to a very large number over a 20–25 year retirement.

Waiting Until 70: The 24% Bonus

For every month you delay claiming past FRA, you earn Delayed Retirement Credits of 2/3 of 1% per month (8% per year). These credits stop accruing at age 70 — there is no benefit to waiting beyond 70. The calculation for three years of delay (67 to 70): 36 months × (2/3)% = 24.00% increase.

At $1,000 PIA, waiting from 67 to 70 produces $1,240/month instead of $1,000/month — $240 more every month, permanently, also growing with COLA each year. At the 2026 COLA of 2.8%, your $1,240 grows by $34.72 per month annually. A 62-year-old claimer's $700 benefit only grows by $19.60 per month at the same COLA rate.

The Break-Even Math: Every Crossover Point

The break-even is calculated by asking: how long does it take for the higher monthly benefit of the later claimer to recover the foregone benefits during the waiting years?

| Comparison | Monthly Advantage | Head Start to Recover | Months to Break Even | Break-Even Age |

|---|---|---|---|---|

| 67 vs 62 | $1,000 − $700 = $300/mo | $700 × 60 months = $42,000 | $42,000 ÷ $300 = 140 months | Age 78 years 8 months |

| 70 vs 67 | $1,240 − $1,000 = $240/mo | $1,000 × 36 months = $36,000 | $36,000 ÷ $240 = 150 months | Age 82 years 6 months |

| 70 vs 62 | $1,240 − $700 = $540/mo | $700 × 96 months = $67,200 | $67,200 ÷ $540 = 124 months | Age 80 years 4 months |

What the average person should know: SSA actuarial tables (2022 period life table) show average male life expectancy at 62 is approximately 81.4 years; for females it is 84.3 years. Both are past the 62-vs-67 break-even of 78y8m — meaning the average person comes out ahead by waiting until at least FRA. Women, who live longer on average, benefit more from delaying to 70.

COLA: Why a Higher Base Means More Dollars Over Time

The 2026 Cost of Living Adjustment is 2.8%, announced by SSA on October 24, 2025. COLA is applied as a fixed percentage to your benefit amount. Because the percentage is the same regardless of your benefit level, a higher base benefit receives larger absolute dollar increases every year.

| Claiming Age | Monthly Benefit ($1,000 PIA) | Annual COLA Increase at 2.8% | Extra Monthly Dollars per Year |

|---|---|---|---|

| 62 | $700 | $19.60/month increase | Baseline |

| 67 (FRA) | $1,000 | $28.00/month increase | +$8.40/month vs age 62 |

| 70 | $1,240 | $34.72/month increase | +$15.12/month vs age 62 |

The Spousal Strategy — and the 2025 Fairness Act

For married couples, the Social Security claiming decision becomes a joint optimization. The key rules:

- A spouse is entitled to up to 50% of the worker's PIA at the spouse's own FRA (67)

- If the spouse claims early at 62, the spousal benefit is reduced to 32.5% of the worker's PIA (using the spousal early retirement reduction formula)

- The spousal benefit does not earn delayed retirement credits — waiting past FRA does not increase the spousal benefit beyond 50% of the worker's PIA

Common household strategy: The lower-earning spouse claims early at 62 or 64 to bring in income, while the higher-earning spouse delays to 70 to maximize their benefit (which also becomes the survivor benefit if the higher earner dies first). This strategy maximizes the higher-earning spouse's survivor protection.

2025 Fairness Act — major change for public employees: The Social Security Fairness Act, signed January 5, 2025, eliminated the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). This affects approximately 3.1 million public employees — teachers, firefighters, police officers, state workers — who also receive pensions from jobs not covered by Social Security. Before this change, their Social Security benefits and spousal/survivor benefits were significantly reduced. As of early 2026, SSA has distributed over $17 billion in retroactive payments (back to December 2023) to eligible beneficiaries. If you or your spouse had benefits reduced by WEP or GPO, contact SSA to verify your updated benefit amount. Source: SSA.gov Fairness Act page.

Decision Framework: When to Claim for Your Situation

| Your Situation | Suggested Strategy | Why |

|---|---|---|

| Healthy, expect to live 80+, no immediate income need | Wait until 70 | Break-even at 82y6m; women average 84y at 62, men 81y — both approach or exceed break-even |

| Healthy, married, higher earner in household | Wait until 70 | Your benefit becomes the survivor benefit; maximizing it protects your spouse for decades |

| Single, uncertain health, expect life expectancy 75–78 | Claim at 65–66 | Below break-even point; earlier claiming produces more total lifetime benefits |

| Need income now, no other retirement assets at 62 | Claim at 62 | Income certainty outweighs the theoretical lifetime advantage of waiting |

| Still working at 62-63 with decent income | Do NOT claim at 62 if working | Earnings test: 2026 threshold = $24,480; SS deducts $1 per $2 earned above limit |

| Public employee with WEP/GPO history (teacher, firefighter) | Re-evaluate with updated benefit | Social Security Fairness Act (Jan 2025) may have substantially increased your benefit |

Earnings test in 2026: If you claim Social Security before FRA while still working, SSA withholds $1 in benefits for every $2 you earn above $24,480 per year. In the year you reach FRA, the threshold rises to $65,160 ($1 withheld per $3 earned above). The withheld amounts are returned as a permanent increase to your benefit once you reach FRA — so it is not lost, but it is deferred. This generally makes early claiming while working a poor strategy. Source: SSA Earnings Test Exempt Amounts (ssa.gov/oact/cola/rtea.html).

Use the UtilsDaily Social Security calculator to model your estimated benefit at different claiming ages and project lifetime totals. For a comprehensive retirement picture, combine it with the savings calculator and net worth calculator.

Sources & Citations

Data sources: SSA.gov — Benefits Planner: Born in 1960 or Later (FRA = 67); SSA.gov — Benefit Reduction for Early Retirement calculator; SSA.gov — Delayed Retirement Credits (8%/year); SSA.gov — Effect of Early or Delayed Retirement; SSA.gov — 2026 COLA Fact Sheet (2.8% effective January 2026); SSA.gov — Social Security Fairness Act (WEP/GPO elimination); SSA.gov — Retirement Earnings Test (2026 thresholds); AARP — Social Security Break-Even Age FAQ (confirms age 78y8m for 67 vs 62); SmartAsset — Social Security Break-Even Age calculator; Benefora.org — Social Security Break-Even Guide 2026; CMS — 2026 Medicare Part B Premiums ($202.90/month); SSA.gov — Actuarial Life Table (2022 period life table).